Contributed Talks

Abstracts of our Talks

Invited Talks

Fred Espen Benth

University of Oslo

Title: A note on cointegration in commodity markets

Abstract: According to the arbitrage theory, cointegration of financial assets will not impact pricing of spread options, as the risk-adjusted returns will be given by the risk-free interest rate. We analyse the similar situation in commodity markets, where typically the market consists of spot, forward/futures and options on these. We show that cointegration in the spot will impact the volatility of forward/futures price dynamics, with the results that spread options indeed will depend on cointegration. Our analysis leads to a Heath-Jarrow-Morton approach with cointegration for forward/futures price modelling in commodity markets.

The talk is based on joint work with Steen Koekebakker, University of Agder.

René Carmona

Princeton University

Title: Financialization of the Commodity Markets: what does it all mean for energy finance?

Abstract: The talk will review the empirical facts at the root of the debate over the financialization of the commodity markets, and some of the arguments used to explain the 'booms and bust' periods at the heart of the controversy. Special attention will be given to natural gas and crude oil as they form a significant component of most of the commodity indexes favored by institutional investors.

Wolfgang Härdle

Humboldt-Universität zu Berlin

Title: Pricing Chinese Rain

Abstract: Many industries are exposed to weather risk which they can transfer to financial markets via weather derivatives. Financial investors and weather exposed business are interested in holding a basket of weather derivatives to manage their risks in an optimal way. We develop a model for pricing such baskets of customized WDs on multiple dependent geographical sites. In our setup, market participants account for spatial dependence in the underlying weather indexes. Dynamic portfolio optimization under market clearing and utility indierence of the agents determines equilibrium quantity and price for weather derivatives. Using the concept of association, we compare our multi-site model to its single-site counterpart. We give an example on how to price rainfall derivatives on Chinese provinces in the universe of a financial investor and weather exposed crop insurance companies.

Sebastian Jaimungal

University of Toronto

Title: Risk and Ambiguity in Real Option Cash-Flows

Abstract: The adoption of real options analysis by industry practitioners remains limited. Managers tend to have a very simplified and condensed view of what potential cash-flows might be and those views are generally at odds with what academic works. For example, approximating cash-flows and/or project values as GBMs or OUs is standard in most academic works, while most practitioners certainly do not have such a model in mind when valuing cash-flows or embedded optionality. Here, we provide a way to incorporate the manager's cash-flow distributions exactly, within an incomplete market setting, using indifference pricing. We will focus on two prototypical options (i) irreversible investment, and (ii) an entry-exit problem, but our approach is quite general. Moreover, we will outline how managers can account for model ambiguity using robust optimization and explore its implications. This is joint work with Yuri Lawryshyn.

Chitro Majumdar

R-square RiskLab

Title: Energy Swap in Gulf States - Changing Patterns

Abstract: Gulf Energy Sector (GES) is faced with great challenges. Nevertheless, GES has to continue to plan and invest over the long-term to provide energy responsibly, reliably, security and safely, and also to constantly balance the economic progress with environmental protection. The national budget of the Gulf States depends in a significant way on the oil and gas price. The market has witnessed a significant upward trend on oil prices as a result of strong market fundamentals and geopolitical tensions. Oil price depends on the demand and on the supply of oil. The supply of oil is not only in correlation with many important factors like finding new resources, shift towards renewables in order to satisfy the huge demand of electricity however it either depends on several uncorrelated variables, which are yet dependent when we consider scenario based climate change and political unrest in MEA (Middle-East Africa) region. Gulf states lead the region in energy efficient building measurement, modeling, and technology development in order to establish building energy baselines, provide energy efficiency guidance, and create tools to facilitate near-term energy savings for building stock that could identify, test, and commercialize technologies to reduce new building energy consumption. The goal would support a gradual replacement of conventional energy sources, such as oil, coal and other fossil fuels, with renewable energy resources, towards a target of renewable energy supplying more than 50 percent of the Gulf's energy needs by next decades.

Finally, a comparative study based case study around the fact that Europe is tending to favor Natural Gas from Eastern frontiers over the Gulf Oil for the reasons attributable to lesser volatility in prices, assured supply and lower environment foot print. There are interesting debates going around the issue in Europe considering the Energy 2020 target.

Luca Taschini

London School of Economics

Title: Pollution permits, Strategic Trading and Dynamic Technology Adoption

Abstract: This paper analyses the dynamic incentives for technology adoption under a transferable permits system, which allows for strategic trading on the permit market. Initially, firms can both invest in low-emitting production technologies and trade permits. In the model, technology adoption and allowance prices are generated endogenously and are inter-dependent. It is shown that the non-cooperative permit trading game possesses a pure-strategy Nash equilibrium, where the allowance value reflects the level of uncovered pollution (demand), the level of unused allowances (supply), and the technological status. These conditions are also satisfied when a price support instrument (dubbed cash-for-permits), which is contingent on the adoption of the new technology, is introduced. Numerical investigation confirms that this policy generates a floating price floor for the allowances, and it restores the dynamic incentives to invest. Given that this policy comes at a cost, a criterion for the selection of a self-financing policy (based on convex risk measures) is proposed and implemented.

This is joint work with Santiago Moreno-Bromberg.

Sjur Westgaard

Norwegian University of Science and Technology

Title: VALUE AT RISK MODELLING USING EXPONENTIAL WEIGHTED MOVING AVERAGE VOLATILITY WITH QUANTILE REGRESSION -An analysis of ICE, ICE-ENDEX, EEX, and Nasdaq OMX Energy Futures Markets-

Abstract: Correct modelling and forecasting of risk for energy futures markets has become an important issue for power companies, industrial companies, and financial institutions exposed to oil, gas, coal, electricity, and carbon markets. As participants in this market have both long and short positions, it is important to model both sides of the tails of the return distributions. It is likely important to take into account how the return distributions changes over time due to changing volatility and market conditions. The problems with existing "standard" risk model such as RiskmetricsTM and Historical simulation are that the former do not capture the changes in the return distribution as the conditional volatility changes, and that the latter have the opposite problem capturing the return distribution but not conditional upon volatility. More advanced GARCH models with different error distributions and CaViaR models where the quantiles itself is modelled as an autoregressive process improves the forecast out of sample but are only to a limited extend used by market participants due to the complexity of estimating these models. In this paper we propose a robust and easy to implement approach for Value at Risk estimation based on first running an exponential weighted moving average volatility model (similar to RiskmetricsTM) and then running a linear quantile regression model based with this volatility as input. The model display excellent in-sample and out-of sample performance compare to a set of benchmark models. We use a wide range of European energy futures markets from ICE, EEX; and Nasdaq OMX covering the period 2006-2013. Each of these markets have very distinct features with different volatility dynamics and distributional characteristics that are captured by the method. The method capture the best of the existing approaches (Riskmetrics and Historical Simulation) and are easy to implement for market risk assessment.

SPONSORS SESSION

Sponsors Session: DEVnet

Speaker: Kim Tang

Topic: Effective Correlation Monitoring of large Data Streams

Abstract: Traders are interested in the correlation of data streams - especially highly correlated pairs. The main interest is to identify highly correlated pairs among tens of thousands data streams using sliding windows in real time. In this talk we will propose efficient methods for solving this problem using Discrete Fourier Transforms.

Sponsors Session: D-fine

Speaker: Magnus Wobben

Topic: Optimization of Trading Strategies in Incomplete Power and Gas Markets

Abstract: The Optimization of trading strategies in power and gas markets has recently become an important issue for both practitioners as well as academics. Due to incomplete spot markets and volume risks, the evaluation and optimization of trading strategies is non-unique and rather depends on the balancing of chances and individual risk preferences. In this talk, we present a universal and practical optimization framework based on the theory of expected utility that overcomes the fallacies of incomplete markets. Practical examples encompass - amongst others - the optimal trading strategy for uncertain Renewable capacities, the optimal usage of gas storage facilities as well as optimal firm-wide transfer pricing.

Sponsors Session: Platinion

Speaker: Stephan Nawracki

Topic: Risk Architectures in the Energy Industry

Abstract: Risk management has become a top priority topic for energy companies. Markets are becoming more liquid and companies acting on these markets are undergoing considerable changes to establish global sales and trading organizations. Thus, there is a clear need to also change a company's mindset towards the own business and in particular to their risk management approach.

In the past 10 years there has already been a clear movement to improve transparency, regulatory guidelines and to manage risk more professionally:

• Enlargement of risk management departments

• Attention and responsibilities up to the top level management

• Utilization of complex risk assessment methods and scenario analysis

However, our daily experience shows that there are still various areas for improvement. A fragmented IT architecture, distributed knowledge and inefficient processes are only some of these areas which can be found in the energy industry.

Yet a consistent concept is often more than just the replacement of IT systems, it can be assumed that the abovementioned improvement areas are only symptoms but not the root cause. Rather it becomes obvious that there is good reason why almost no company has reached the desired level of transparency in risk and why there is still a huge gap between theory and practice.

In order to identify possible root causes for these symptoms and to understand the reasons behind the current situation in energy companies, Platinion conducted interviews with key players from leading energy companies, vendors and risk experts. The interviews were focusing on three main areas, namely:

• IT and business architecture regarding risk management

• Risk indicators and reporting

• Operations in IT and risk departments

As a result of these interviews and their analysis, three main hypotheses on possible root causes have been identified and will be presented in the given session. In addition there will be an in depth presentation of interview results and the proposal of possible solution options to mitigate symptoms and to address the identified root causes.

The presentation is meant for risk practitioners and auditors from the energy sector, as well as academics who are interested in the current state of the art in practice.

Sponsors Session: RWE SUPPLY & TRADING

Speaker: Thomas Pieper

Topic: Challenges of Power Price Forecasting

CONTRIBUTED TALKS

Gülsüm Akarsu

Title: The effect of economic volatility on electricity demand: Panel data analysis for turkey

Abstract: The effect of volatility on economy has been widely discussed by the previous studies both theoretically and empirically. In this study, our purpose is to analyse the effect of volatility associated with some important economic variables on electricity demand, as well as, to determine the factors that influence the electricity consumption for Turkey using annual balanced panel data on 65 provinces over the period between 1990 and 2001. In this context, we build a dynamic panel data model in which electricity consumption is modelled as a function of per capita gross domestic product, electricity end-use prices, urbanization ratio, heating degree days, cooling degree days, and volatility. As a proxy for volatility, we employ conditional variance of real exchange rate growth, conditional variance of industrial production index growth, conditional variance of crude oil price growth, conditional variance of nominal exchange rate growth and conditional variance of İstanbul Stock Exchange-100 index growth which are all obtained from the estimations of various GARCH models. The estimation of the dynamic panel data model is performed by employing system GMM suggested by Blundell and Bond (1998) under the assumption of homogeneous slope coefficients and error variances across the provinces. We find that among the volatility measures, only industrial production volatility has a statistically significant and positive effect on electricity consumption. Further, our results indicate statistically significant and theoretically consistent effects of income, electricity price, and urbanization ratio. Lastly, findings show that electricity demand is inelastic with respect to income and price implying that the pricing policies may not be so much effective to decrease electricity demand and also, low income elasticity may be the reflection of low energy intensity showing efficient use of energy. As policy recommendation, we suggest restructuring of the industrial sector to the less-energy intensive structure, extensive energy efficiency programs, and supporting generation capacity expansion and pricing policies by the diversification across energy resources.

The talk is based on joint work with Esma Gaygısız.

Stefan Ankirchner

Title: Hedging forward positions: basis risk versus liquidity costs

Abstract: Consider an agent with a forward position of an illiquid asset (e.g. a commodity)

that has to be closed before delivery. Suppose that the liquidity of the asset increases as the delivery date approaches. Assume further that the agent has two possibilities for hedging the risk inherent in the forward position: first, he can enter customized forward contracts; second, he can acquire standardized and liquidly traded forward contracts. We assume that purchasing customized forwards perfectly eliminates the risk, but entails high liquidity costs charged by the counterparty. The standardized forwards can be acquired at considerably lower costs, but do not perfectly match the agent's risk and hence entail basis risk. By means of stochastic control we show how to obtain an optimal trade-off between liquidity costs and basis risk. To this end we reduce the hedging problem to a family of stopping problems. In two case studies we consider simple liquidity dynamics for which optimal hedging strategies can be calculated explicitly.

The talk is based on joint work with Peter Kratz and Thomas Kruse.

Thjs Benschop

Title: Volatility Modelling of CO2 Spot Prices Using Markov Switching Models

Abstract: We analyse the short-term spot price of European Union Allowances (EUAs), which is of particular importance in the transition of energy markets and for the development of new risk management strategies. We use daily spot market data from the second trading period of the EU ETS. Emphasis is given to short-term forecasting of prices and volatility. Due to the characteristics of the price process, such as volatility modelling, breaks in the volatility process and heavy-tailed distributions, we investigate the use of Markov switching GARCH (MS-GARCH) models. We find that these models distinguish well between states, and that the volatility processes in the states are clearly different. Our findings support the use of MS-GARCH models for risk management, especially because their forecasting ability is better than other Markov switching or simple GARCH models.

The talk is based on joint work with Brenda López Cabrera.

Sara Ana Solanilla Blanco

Title: Forward prices as functionals of the spot path in commodity markets modeled by lévy semistationary processes

Abstract: We show that the forward price can be represented as a functional of the spot price path in the case of Lévy semistationary models for the spot dynamics. The functional is a weighted average of the historical spot price in general, and is derived by means of the Laplace transform. We focus our interest in a special case of Lévy semistationary processes known as Continuous-time autoregressive moving average processes (CARMA) which are of interest in energy price modeling and provide a discussion of the results based on numerical examples.

The talk is based on joint work with Fred Espen Benth.

Svetlana Borovkova

Title: News, volatility and jumps: the case of Natural Gas futures

Abstract: We investigate the impact of Thompson Reuters News Analytics (TRNA) news sentiment on the price dynamics of natural gas futures traded on the New York Mercantile Exchange (NYMEX). We propose a Local News Sentiment Level (LNSL) model, based on the Local Level model of Durbin and Koopman (2001), to construct a running series of news sentiment on the basis of the 5-minute time grid. Additionally, we construct several return and variation measures to proxy for the fine dynamics of the front month natural gas futures prices. We employ event studies and Granger causality tests to assess the effect of news on the returns, price jumps and the volatility.

We find significant relationships between news sentiment and the dynamic characteristics of natural gas futures returns. For example, we find that the arrival of news in non-trading periods causes overnight returns, that news sentiment is Granger caused by volatility and that strength of news sentiment is more sensitive to negative than to positive jumps. In addition to that, we find strong evidence that news sentiment severely Granger causes jumps and conclude that market participants trade as some function of aggregated news.

We apply several state-of-the-art volatility models augumented with news sentiment and conduct an out-of-sample volatility forecasting study. The first class of models is the generalized autoregressive conditional heteroskedasticity models (GARCH) of Engle (1982) and Bollerslev (1986) and the second class is the high-frequency-based volatility (HEAVY) models of Shephard and Sheppard (2010) and Noureldin et al. (2011). We adapt both models to account for asymmetric volatility, leverage and time to maturity effects. By augmenting all models with a news sentiment variable, we test the hypothesis whether including news sentiment in volatility models results in superior volatility forecasts. We find significant evidence that this hypothesis holds.

The talk is based on joint work with Diego Mahakena.

Roel Brouwers

Title: The impact of EU ETS verification events on stock prices

Abstract: In this study we investigate how the publication of verified emissions in the European Emissions Trading Scheme (EU ETS) affected stock prices of covered companies. Based on a unique sample of 368 listed companies located in 25 countries, the event study results demonstrate that 2 out of 6 publication events over the period 2006-2011 resulted in statistically significant market responses. The two significant events were the first publication of verified emissions in the first phase, a pilot period that ran from 2005 to 2007, and the first publication in the second phase, coinciding with the Kyoto Protocol commitment period and comprising the years 2008 to 2012. These findings indicate that investors value particularly the information revealed at the first verification event of each EU ETS phase and that subsequent verification events are less informative. The cross-section analysis of abnormal returns surrounding the publication of verified emissions reveals a positive correlation between the market reaction and the level of excess allowances. Contrary to expectations, we find no evidence of a negative association between unanticipated verified emissions and abnormal returns.

The talk is based on joint work with Frederiek Schoubben, Cynthia Van Hulle and Steve Van Uytbergen.

Che Mohd Imran Che Taib

Title: Forward pricing in the shipping freight market

Abstract: In this paper, we derive the price of the forward freight contract using spotforward relationship framework. We base our pricing on six different stochastic models which can capture many stylized facts of spot freight rates such as heavy-tailed logreturns, time-varying volatility and mean reversion. The models are analytically tractable which allows for pricing of forwards. We also examine the shape of forward curve for all continuous-time forward pricing formulas and find various shapes being the combination of fixed and stochastically dependent terms. Finally, this paper discusses the effect of different time to delivery and the maturity effect to the forward curve.

David G. Stack

Title: Natural Gas and Crude Oil in Europe: Have they decoupled?

Abstract: The deregulation of energy commodity markets, which has been underway in Northern Europe since the mid-90's, has caused changes in the dynamics of the principal EU energy markets, and their representative benchmarks.

One major aim of deregulation is to allow markets to respond to supply and demand conditions, this has been particularly true in the electricity and natural gas markets where prices are determined by market participants more than by regulators. A more competitive market for electricity, for example, suggests that its spot prices will promptly respond to price changes in input fuels.

Many scholars, using different dataset and methodologies, have investigated whether natural gas and crude oil prices are related. Market behavior in the 90's suggested that changes in the oil price drove changes in the natural gas price, and that the converse did not occur. In the past decade the relationship between oil and gas has been increasingly affected by the various deregulating policies and the introduction of new technologies.

For some scholars oil prices are expected to remain the long run driver of energy price dynamics through inter-fuel competition and price indexation clauses, from a Dynamic Commodity Trading perspective there is no a priori expectation of a sustaining relationship between oil and natural gas.

Better understanding of the relationship between crude oil and the natural gas market in Europe is a crucial issue for risk management strategies and to appreciate the efficacy of government policies aimed to create true competitive markets.

The European Third Energy Package aspires to create a unique gas and electricity market for the entire zone. The anticipation, announcement and implementation of the Third Package has had different effects on each of the EU's major gas hubs during a time when Brent has changed its index structure and become "the major index" for crude oil benchmark in the world. In the last decade 7 European hubs have become increasingly active and give us a better data set to investigate possible relationships between oil and gas.

Following a critical review of developments in:

1. the EU's supply and demand for Natural Gas;

2. the change in LNG role in the EU;

3. the geopolitics of Russia, as the historical major supplier to the EU zone;

4. the change in market structure, design and its dominant players

5. the EU's Third Package and in particular the Gas Target Model.

We study daily price levels and price changes, as well as forward curves for each of the seven European Hubs and for Brent. With the daily price data for the period 2005-2013 in the seven principal different European gas hubs and Brent we measure a possible relationship between the two commodities. The Error Correction Model (ECM) framework is used to measure the dynamics of this relationship. A Rolling correlation estimate as well as an Engle Granger representation is used to investigate a possible short run relationship.

We try to address the recently debated role of speculation and financialization in the changing structure of price volatility which occurred in these markets. We further discuss the role of changing regulation to understand the recent price dynamics.

We believe our study has important ramifications for investment decisions of both private firms and utilities as well as the direction of future energy policy.

The talk is based on joint work with Rita D'Ecclesia.

Nikolai Dokuchaev

Title: Continuously controlled options and related first order backward SPDEs

Abstract: We introduce a continuous time extension of swing options and Asian options such that the holder selects dynamically a continuous time process controlling the distribution of the payments (benefits) over time. For instance, the holder can select dynamically the quantity of a commodity purchased or sold by a fixed price given constraints on the cumulative quantity. The pricing of these options requires to solve special stochastic control problems with constraints for the cumulative control similar to a knapsack problem. Some existence results and pricing rules are obtained in Markovian and non- Markovian setting.

In Markovian setting, diffusion HJB equations are derived. In non- Markovian setting, a backward stochastic partial differential equation of a new type is derived for the value function of swing options; this part of the presentation is based on joint work with Christian Bender (Saarland University).

Paolo Falbo

Title: Design of efficient cap-and-trade systems: An equilibrium analysis

Abstract: The European Union Emissions Trading Scheme (EU ETS) has arrived at the third phase, with several adjustments being applied to improve its effectiveness. For example, after having been vastly criticized in the literature, the grandfathering of the certificates to the firms involved in the system has been finally strongly reduced, especially for the electricity generation industry. Nevertheless, several other critical aspects are still in place risking to hamper the main objective that the EU ETS is supposed to achieve: a socially sustainable and economically efficient reduction of the emissions of greenhouse gases. In a relatively recent document (see [1]), the EU commission recognizes the urgency to cope with the problem of an excess of allowances circulating in the market, in order to keep the price sufficiently high to trigger CO2 reduction investment. Among others, the following structural measures are envisaged in this document:

- introducing a discretionary price management mechanism,

- extending the scope of the EU ETS to other sectors,

- retiring a number of allowances in phase three.

Such solutions are deeply different in the method to face the problem. They witness some lack of vision on the side of the EU Commission and especially an insufficient care in addressing some fundamental aspects of the system, such as correctly sizing the number of certificates to be issued during the previous and the current phases.

Also the comments from the political side have been raising in the criticism towards EU ETS (see [2]), to a level that has arrived to doubt in some cases even if this system is worth to survive. Before that extreme solutions introduce more problems than they are intended to remove, it is important to get a clear understanding of the full potential benefits of the environmental markets based on a capand-trade principle, such as EU ETS, and to get a clear vision of what is at the origin of the drawbacks experienced so far, trying to gain insights on how to calibrate appropriate measures. This paper is aimed to contribute to this purpose.

The efficiency properties of environmental markets have been first addressed in [3] and [4], who first advanced the principle that the "environment" is a good that can not be "consumed" for free. In particular, Montgomery describes a system of tradable certificates issued by a public authority coupled with fixing a cap to the total emissions, and, doing so, to force polluting companies paying proportionally to the environmental damage generated by their production activity. An emission certificate is representative of the permission to emit a given quantity of pollutant without being penalized.

Less polluting companies can sell excess certificates, the resulting revenue represents a general incentive to reduce pollution. Montgomery shows that the equilibrium price for a certificate must be driven by the cost of the most virtuous company to abate its marginal unit of pollutant. The key result of his analysis however is that such a system guarantees that the reduction of pollution is distributed among the companies minimizing the total costs. This is equivalent to achieving the environmental protection in the most cost-efficient way.

After the seminal analysis of Montgomery, which is based on a deterministic and static model, the following research has taken the direction to the stochastic and multi-period settings. A literature review on the research which has developed after Montgomery's work can be found in [5]. A common result shared by all the understanding reached so far is that the cap-and-trade systems indeed represent the most efficient way to reduce and control the environmental damage generated by the industrial activity.

Let us mention now the contributions which are directly related to our analysis. A majority of relatively recent papers (e.g. [6]; [7]; [8]; [9]; [10]; [11]; [12]; [13]; [14]) are related to equilibrium models, where the individuals optimize their profit or cost function. In particular, combining equilibrium arguments with modelling of individual cost structure, social optimality and optimal market design of a cap-and-trade system is addressed in [11]. However, this work significantly simplifies the framework by assuming linear utility functions for all agents, which neglects risk aversion aspects.

The main purpose of this work is to show within a risk averse market model, that an environmental market combines two contrasting aspects: on one hand, the emission trading provides a cost efficient way to reach pollution reduction, in line with the existing research results. On the other hand, we show that, although the costs of emission savings are in certain sense minimal, the distribution of the social burden among individuals is unequal. In the generic market design, the emission regulations may result in significant excess revenue of the producers, whereas the consumers pay far more that the costs of the emission reduction.

To prove these two properties, we consider a simplified single-period setting and assume that agents (in particular electricity producers) seek to maximize the expected utility of their terminal wealth finding an equilibrium price of emission certificates. In this framework we define and prove social cost-efficiency of a cap-and-trade mechanism. Furthermore, we show that the so-called cost-passthrough is inherent to each emission trading scheme and explain why this property necessarily leads to a notable wealth transfer from consumer to producer, although the overall costs of emission reduction are minimized at the same time.

An important issue must be underlined at this point. The social optimality obtains with respect to an artificial, the so-called risk-neutral, measure. Economically, this could be interpreted as if the "invisible hand" of Adam Smith, which optimizes the allocation of resources, is endowed with a probability different from the objective. In this sense, our findings show that, due to regulation, the decisions of risk averse individual producers on shifting production towards cleaner technologies collectively appear as if they were driven by a superior administrator, who follows a plan for the entire society, optimized from a risk-neutral perspective.

Being first introduced as a pricing vehicle in financial mathematics, the stochastic modeling with respect to risk-neutral measure proves to be a powerful method also to model more general equilibrium problems.

1] E. Commission, Report from the commission to the European Parliament and the Council - the state of the European carbon market in 2012, Tech. Rep. COM(2012) 652 final, European Commission, Brussels, Belgium (2012).

[2] J. Stonington, Is Europe's emissions trading system broken?, Spiegel Online International October 26 - 1:07 PM.

[3] J. H. Dales, Land, water, and ownership, The Canadian Journal of Economics 1 (4) (1968) 791- 804.

[4] W. D. Montgomery, Markets in licenses and e-cient pollution control programs, Journal of Economic Theory 5 (3) (1972) 395-418.

[5] L. Taschini, Environmental economics and modeling marketable permits, Asia-Pacific Financial Markets 17 (4) (2010) 325-343.

[6] B. Stevens, A. Rose, A dynamic analysis of the marketable permits approach to global warming policy: A comparison of spatial and temporal exibility, Journal of Environmental Economics and Management 44 (1) (2002) 45-69.

[7] M. Chesney, L. Taschini, The endogenous price dynamics of the emission allowances and an application to CO2 option pricing, Swiss Finance Institute Research Papers 08-02, Swiss Finance Institute, Zurich, Switzerland (2008).

[8] J. Seifert, M. Uhrig-Homburg, M. Wagner, Dynamic behavior of CO2 spot prices, Journal of Environmental Economics and Management 56 (2) (2008) 180-194.

[9] P. Barrieu, M. Fehr, Integrated EUA and CER price modeling and application for spread option pricing, Centre for Climate Change Economics and Policy Working Papers 50, Centre for Climate Change Economics and Policy, London, UK (2011).

[10] R. Carmona, M. Fehr, J. Hinz, Optimal stochastic control and carbon price formation, SIAM Journal on Control and Optimization 48 (4) (2009) 2168-2190.

[11] R. Carmona, M. Fehr, J. Hinz, A. Porchet, Market design for emission trading schemes, SIAM Review 52 (3) (2010) 403-452.

[12] R. Carmona, M. Fehr, The clean development mechanism and joint price formation for allowances and CERs, in: R. Dalang, M. Dozzi, F. Russo (Eds.), Seminar on Stochastic Analysis, Random Fields and Applications VI, Vol. 63 of Progress in Probability, Springer Basel, 2011, pp.

341-383.

[13] J. Hinz, A. Novikov, On fair pricing of emission-related derivatives, Bernoulli 16 (4) (2010) 1240-1261.

[14] M. Kijima, A. Maeda, K. Nishide, Equilibrium pricing of contingent claims in tradable permit markets, The Journal of Futures Markets 30 (6) (2010) 559-589.

This talk is based on joint work with Juri Hinz and Cristian Pelizzari.

Stein-Erik Fleten

Title: Keeping the Lights On Until the Regulator Makes Up His Mind

Abstract: The purpose of this paper is to examine empirically the real options to shutdown, startup, and abandon existing production assets using detailed information for 1,121 individual power plants for the period 2001–2009, a total of 8,189 plant-year observations. We find strong evidence of real options effects. We find that uncertainty about the outcome of ongoing deregulation in retail electricity markets (i) decreases the probability of shutting down operating plants, and, (ii) decreases the probability of starting up plants which were previously shutdown.

The talk is based on joint work with Erik Haugom, Carl Ullrich.

Martin Hain

Title: Risk Factors and Their Associated Risk Premia: An Empirical Analysis of the Crude Oil Market

Abstract: This paper investigates the role of volatility and jump risk for the pricing and hedging of derivative instruments and quantifies their associated risk premia in the U.S. crude oil futures and option markets. To capture the joint dynamics of futures and option prices, we estimate the volatility and jump processes using historical return data and synthetic variance swap rates simultaneously. This avoids potential inconsistencies of multistage estimation approaches and increases the robustness of parameter estimates significantly. Our estimation results show that jump risk is priced with a significant premium, while no evidence for a significant market price of volatility risk exists. In addition, we test the pricing and hedging performances of the different model specifications. The pricing errors show that both volatility and price jump risk are required to capture strongly fluctuating implied volatility levels and pronounced implied volatility smiles. The hedging results further show that an active management of volatility risk significantly reduces the risks of hedge portfolios, while unhedgeable jump risk is required to capture the tail risk of hedge portfolios adequately.

The talk is based on joint work with Marliese Uhrig-Homburg, and Nils Unger.

Stefen Hitzemann

Title: Empirical Performance of Reduced-Form Models for Emission Permit Prices

Abstract: The design of environmental trading systems induces specific features of the emission permit price dynamics. In this paper, we evaluate the performance of reduced-form models for emission markets that capture these features in a simplified way and are still feasible for calibration to permit spot, futures, and option prices. Using market data from the European Union Emissions Trading System as the world's largest environmental market, we show that appropriately specified reduced-form models outperform standard approaches with respect to both the historical t to futures prices and the option pricing performance. Moreover, the performance of reduced-form models critically depends on their consistency with the design of the emission trading system.

The talk is based on joint work with Marliese Uhrig-Homburg.

Melanie A. Houllier

Title: Germany´s Energy Transition and European Electricity Market Integration

Abstract: The German Energiekonzept (Energy Concept) was proposed in 2010 with the goal of making the country one of the world's most energy efficient and environmentally friendly economies (Bundesregierung, 2011). One year later, as a reaction to the multiple reactor meltdowns in Fukushima, this strategy was reinforced with a broad consensus within the German government to implement its Atomaustiegsgestz (Nuclear Phase-Out Act), by closing immediately eight nuclear power plants and then the remaining nine until 2022 (Bundesregierung, 2011). Subsequently, the Renewable Energy Source Act 2012 (RESA, 2012) aims to increase electricity generated from renewable sources to at least 35% by 2020 and to at least 80% by the year 2050. In this context this paper examines long run and short run associations between European electricity markets. We examine the potential impact of wind generated electricity produced in Germany on other European electricity markets, by employing MGARCH (multivariate generalized autoregressive conditional heteroscedasticity) models with constant and time-varying correlations for daily data as well as a semiparametric time varying fractional cointegration analysis. The short run interrelationship of electricity spot prices of APX-ENDEX (UK and Netherlands), Belpex (Belgium), EPEX (Germany and Switzerland), OMEL (Spain and Portugal), Nord Pool (Finland, Denmark and Norway), Ipex (Italy), OTE (Czech) and Powernext (France) with wind penetration induced by the German system is studied from November 2009 to October 2012, thus covering the period before and after the closures of eight nuclear power plants. The long run associations are studied from 2006 to 2009 with mean average week daily data of the same markets.

The talk is based on joint work with Lilian M. de Menezes.

Ronald Huisman

Title: Renewable Energy and Electricity Prices: Indirect Empirical Evidence from Hydro Power

Abstract: Many countries have introduced policies to stimulate the production of electricity in a sustainable or renewable way. Theoretical and simulation studies provide evidence that the introduction of renewable energy promotion policies lead to lower electricity prices as sustainable energy supply as wind and solar have very low or even zero marginal costs. Empirical support for this result is relatively scarce.

The motivation for this study is to provide additional empirical evidence on how the growth of low marginal costs renewable energy supply such as wind and solar influences power prices. We do so indirectly studying Nord Pool market prices where hydro power is the dominant supply source. We argue that the marginal costs of hydro production varies depending on reservoir levels that determine hydro production capacity. Hydro power producers have an option to produce or to delay production and the value of the option to delay increases when the reservoir levels decrease and the option to delay decreases in value when reservoir levels increase and producers face the risk of spillovers. Hence, an increase in reservoir levels mimics the situation of an increase of low marginal costs renewable energy in a market. Our results show that higher reservoir levels, more hydro capacity, lead to significant lower power prices. From this we conclude that an increase in low marginal costs renewable power supply reduces the power prices.

The second contribution of this paper is that we develop a market clearing price model by modeling the supply curve of power that varies over time depending on fundamentals such as hydro capacity and the prices of alternative power sources and that deals with maximum prices which apply to all power markets that we know.

With our result, we strengthen support for the view that an increase in wind and solar supply lowers the power price. This is good news for consumers, but it increases the costs of sustainable energy policies such as feed-in tariffs and at the same time lowers revenues and profits for power producers in case governments would abandon such policies. This effect makes the economic and policy support for renewable energy less sustainable. Policy makers have to account for this if they want to stimulate a sustainable growth of sustainable energy supply.

The talk is based on joint work with Victoria Stradnic and Sjur Westgaard.

Mehtap Kilic

Title: Electricity futures prices: time varying sensitivity to fundamentals

Abstract: This paper analyses the time varying impact of underlying fossil fuels such as coal and natural gas, as well as carbon emission allowance forward prices on the forward electricity price formation over the trading period of a calendar contact. To capture the dynamics in the price formation we apply the univariate unobservable component model in which the explanatory variables are functions of time and the parameters are time varying. We expect that at the beginning of the trading period of a forward power contract the price will be determined by the forward fuel price of the marginal fuel with the lowest cost and when the 'to be' hedged capacity of the plants with the lowest marginal cost is almost met, the forward price will be determined by the next marginal fuel in line. For this we examined the base, peak and off-peak forward prices of the calendar 2013 contract from the German market (EEX) in which the power production is mainly based on the fossil fuels coal and natural gas. We observe that the sensitivities of long term electricity futures prices to explanatory variables coal and natural gas vary over time according to the merit order. This behaviour of power prices has clear implications for the valuation and hedging of forward contracts during the trading period.

The talk is based on joint work with Stein-Erik Fleten, Ronald Huisman, Enrico Pennings and Sjur Westgaard.

Nicolas Koch

Title: Tail events: A New Approach to Understanding Extreme Energy Commodity Prices

Abstract: This paper shows that extreme energy price changes, located in the 10% tails of the distribution, cluster across energy futures markets during the boom-bust cycle of 2006 to 2012. Using multinominal logit regressions, I find that the coincidence of such tail events cannot be explained solely by common supply and demand fundamentals. Instead, I provide evidence that the transmission of extreme price changes occurs through a financial demand channel. Specifically, changes in the net long position of hedge funds are associated with a significant increase in the probability of coincident large positive and negative returns across energy markets. Evidence that index investments drive tail events is limited. Further, I identify adverse shocks to speculator funding liquidity as determinant of synchronized price drops across energy markets. The likelihood of extreme negative returns in more than one market significantly increases when the TED spread rises.

Sascha Kollenberg

Title: Governmental Intervention on Carbon Markets: Weak Target Zones and Stochastic Optimization

Abstract: Under a cap-and-trade scheme, the permit price signal that emerges from the quantity restriction drives technological adoption. In the short-term, unexpected shifts in permits demand can produce significant price trend variation. In the long run, the ups and downs of allowance prices can play a beneficial countercyclical role. Yet, a significant supply-demand imbalance can seriously undermine the orderly functioning of the allowance market. Recently, the price of permits in the European Union Emission Trading Scheme has fallen to a level that could damage not just Europe's low-carbon ambitions but the credibility of the ETS itself. Recent debate reforming the EU ETS spawns a number of open questions related to policy design with numerous similarities to the target zones in exchange rate.

One interesting problem is the credibility of the enforcement mechanism. First, we introduce the concept of a target zone where pre-announced bounds are weakly defended and determine the optimal intervention policy. Second, we show that the presence of the so-called "honey-moon" effect reduces the volume of required intervention. We construct an illustrative model which yields intuitive closed-form solutions for both the optimal intervention policy and the resulting price process. The latter allows a straightforward calculation of the confidence intervals of the pre-announced weak target zone. These preliminary findings pave the way for future research on rule-based management mechanisms and on the market reactions to policy intervention in the framework of stochastic games.

This talk is based on joint work with Luca Taschini.

Paul Krühner

Title: On Forward Modelling In Electricity Markets: An infinite Dimensional Stochastic Analysis Perspective

Abstract: The Heath Jarrow Morton approach treats the family of forwards as primary assets and models them directly. This approach has been used for the modelling of forward prices in electricity markets by several authors and it has found its use by practitioners. We follow this approach and investigate some implications on forwards and spot from an infinite dimensional point of view. Denoting the spot price by S(t) the forwards are defined by

f(t,x):= E(S(t+x)|F_t), x,t > 0

Due to the Heath Jarrow Morton Musiela drift condition the dynamics of f(t) cannot be specified arbitrarily under the pricing measure. We model it by

df(t,x) = d/dx f(t,x) dt + R(t)dL(t,x)

in a suitable function space where L is some Lévy process. In this setting we find representations for the correlation between forwards in standard parametrisation, we find that the spot is necessary a Volterra process and we show that any of such models can be represented as a sum of Ornstein-Uhlenbeck type processes.

This talk is based on joint work with Fred Espen Benth.

Michael Kustermann

Title: A Structural Model for Interconnected Electricity Markets

Abstract: Structural or hybrid models have become very popular to model electricity spot prices due to the fact that risk factors driving supply and demand are better understood and easier observable than in most other markets. However, one very important risk factor - import and export - could not be modeled endogenously in such a model. We propose a multi-market extension of the class of Structural models which is able to capture the subtle interplay between separated but interconnected electricity markets.

Nina Lange

Title: Energy Quanto Options

Abstract: In energy markets, the use of quanto options have increased significantly in the recent years. The payoff from such options are typically triggered by an energy price and a measure of temperature and are thus suited for managing both price and volume risk in energy markets. We propose to write these contracts on energy and weather futures, such that we using an HJM approach can derive closed form option pricing formula for energy quanto options, under the assumption that the underlying asset prices are log-normally distributed. This approach encompasses several interesting cases, such as geometric Brownian motions and multifactor spot models.

Frank Lehrbass

Title: Coping with the Clearing Obligation - from the Perspective of an Industrial Corporate with a Focus on Commodity Markets

Abstract: The European Markets Infrastructure Regulation (EMIR) allows to burden a clearing obligation on nonfinancial corporates, which formerly did not necessarily clear their business. We give ten recommendations on how to cope with this obligation. These are motivated by a case study for which we consider a stylized German power producer. For this entity we derive optimal levels of planned production and forward sales of power using micro-economic theory. Since this results in a significant short position in the German power forward market, we investigate the resulting variation margin call dynamics with a special interest in the ability to forecast worst case price upmoves. We compare different models for the forward log returns and their performance in 99% quantile forecasting. A GARCH model with Student-t distribution emerges as the most suitable model. This is used in the case study, which is inspired by data published by the power producer E.ON. Using recent material from the Basel Committee on Banking Supervision we distill the reliable liquidity buffer from an allegedly rich liquidity position and show how suddenly it can be eroded. We point to feedback loops, which make the challenges - posed by the clearing obligation - even more severe.

Brenda Lopez Cabrera

Title: Pricing rainfall futures at CME

Abstract: Many business people such as farmers and financial investors are affected by indirect losses caused by scarce or abundant rainfall. Because of the high potential of insuring rainfall risk, the Chicago Mercantile Exchange (CME) began trading rainfall derivatives in 2011. Compared to temperature derivatives, however, pricing rainfall derivatives is more difficult. In this article, we propose to model rainfall indices via a flexible type of distribution, namely the normal-inverse Gaussian distribution, which captures asymmetries and heavy-tail behaviour. The prices of rainfall futures are computed by employing the Esscher transform, a well-known tool in actuarial science. This approach is flexible enough to price any rainfall contract and to adjust theoretical prices to market prices by using the calibrated market price of risk. The empirical analysis is conducted with US precipitation data and CME futures data providing first results on the market price of risk for rainfall derivatives.

Carlo Lucheroni

Title: Thermal and Nuclear Energy Portfolio Selection using LCOE CVaR

Abstract: Investment decisions and assessment in electricity production are usually supported by a Levelised Cost of Energy (LCOE) analysis. For a firm owning a portfolio of generating assets, this approach determines the minimum selling price PLCOE of the electricity produced by its generation technologies mix that is necessary to cover all operating expenses, interest and principal repayment obligations on the debt incurred for the assets investment, taxes, and to provide equity investors the adequate return for the assumed risk. This last return is quantified by the Weighted Average Cost of Capital (WACC) rate. More precisely, PLCOE is determined as the price at which discounted costs and electricity sale revenues are equal, i.e. as a break-even price. In a stochastic dynamic approach, PLCOE can then be seen as a stochastic variable with an expected value and a variance, so that the volatility of operating costs like fuel price volatility are then reflected in these expectations. LCOE is then computed as the PLCOE expectation, an LCOE variance can be defined, and this LCOE variance will take into account fuel prices variance. Applying this methodology, different portfolios and investment strategies can be compared by comparing their corresponding levelized costs, and portfolios optimal under given objectives can be selected by choosing optimal technology mixes. For firms endowed by thermal technologies like gas and coal, an important cost can come from CO2 abatement market purchases, where compulsory. In this case, if the portfolio optimality objective includes minimum LCOE variance, besides taking into account the volatility of thermal fuels prices, direct and indirect impact of CO2 prices must be considered in the computation of LCOE and its variance.

In [1] such an approach was taken to study the effect of adding nuclear power to an otherwise purely thermal technology mix portfolio, computing minimum LCOE variance portfolios along scenarios where CO2 prices volatility increases. Production of electricity by means of nuclear plants doesn't generate CO2, so that inclusion of this asset in a generation portfolio has the same diversifying effect as a risk free bond in an equity portfolio. As the level of CO2 prices volatility increases, one of the results discussed in [1] is the prescription of how much nuclear power minimum LCOE. variance portfolios should include. The numerical outcome is not immediately evident, since it depends on the WACC rate with which LCOE is computed, i.e. by the stance investors have on the riskiness of the nuclear business. The analysis carried out in [1] elucidates how these two 'environmental' risks, nuclear business risk and CO2 prices volatility, compete in the decision of setting how much weight to give to nuclear assets in a thermal energy minimal variance portfolio which can include the nuclear option.

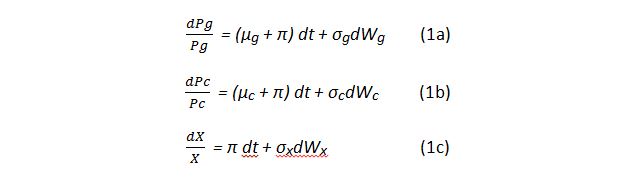

Since Ref. [1] was concentrated on the formal developement of the discussed assessment methodology, the continuous time model dynamics chosen for the gas Pg(t), coal Pc(t), and CO2 X(t) price series were simple standard geometric brownian motion diffusions of the form

where π = ln(1 + i), i is the expected inflation rate, µg and µc are related to the real escalation rate of the corresponding fuel prices, σg, σc and σx are the price volatilities, Wg, Wc and Wx are independent Wiener processes. Whereas in some contexts the processes in Eqs. (1a) and (1b) can be considered reasonable assumptions to describe fossil fuels prices dynamics [2], Eq. (1c), they can be considered as a starting point to model the much more complicated financial risk involved both in fossil fuel prices and in CO2 emissions trading. To take this into account, and to make the analysis more accurate, in this paper a richer mean-reverting Lévy model describing the time evolution of fossil fuels prices and CO2 prices will be studied. For each variable, the dynamics can be chosen according to the following jump-diffusion form

where Y is the natural logarithm of the market prices of fossil fuels or CO2 prices. Switching from Eq. (1c) to Eq. (2) implies though a much larger financial tail risk, which is not well captured by variance. CVar, a risk measure more sensitive to the shape of the tail of the PLCOE distribution, can then be used in a more reliable scheme of portfolio selection, in which a minimal CVar portfolio is computed.

1) C. Mari, Hedging Electricity Price Volatility using Nuclear Power, to be published in Applied Energy, 2014.

2) M. T. Hogue A Review of the Costs of Nuclear Power Generation, BEBR, University of Utah, 2012.

This talk is based on joint work with Carlo Mari.

Reinhard Madlener

Title: Hydrogen Storage for Wind Parks - A Real Options Evaluation for Optimal Investment in Flexibility

Abstract: In this paper we investigate the economic viability of hydrogen storage for excess electricity produced in wind power plants. To this end, we define two scenarios and use both Monte-Carlo simulation and real options analysis. The use of hydrogen as a storage medium helps to increase capacity utilization of the wind parks; in case of disconnection of the wind park (grid overload, grid stability considerations), the investor can also offer system-relevant services by producing reserve energy. It also allows temporal arbitrage, i.e. to purchase electrical energy at low spot market prices for generating hydrogen and to sell electricity that is generated from hydrogen at high spot market prices. Finally, system services can be offered in the form of minute reserve.

This talk is based on joint work with Daniel Kroniger.

Christian Maxwell

Title: Using Real Option Analysis to Quantify Ethanol Policy Impact on Production

Abstract: Ethanol crush spreads are used to model the value of a facility which produces ethanol from corn. A real options analysis is used to investigate the effects of energy policy on management's decision to operate the facility through optimal switching and the firm's decision to enter into the project. We perform the analysis using PDE techniques by means of a layered stochastic optimal control problem via optimal exercise into a switching problem. We present evidence of increased correlation between corn and ethanol prices, perhaps as a result of government policy which has induced more players to enter into the market. This talk investigates the subsequent negative impact on valuations. Further, this talk illustrates the impact of policy uncertainty via a stochastic process which models the possibility of a future abrupt change in government policy on a firm's decision to enter the business.

Anna Nazarova

Title: Model Risk in Energy Markets

Abstract: Recently, model risk, in particular parameter uncertainty, has been addressed for financial derivatives. During this talk we will review these concepts and apply the methods to energy markets. In particular, we will discuss parameter uncertainty for spread options and implications for fossil power plant valuation. To capture model risk we use a methodology recently established in a series of papers by Bannör and Scherer. As gas-fired power plants are seen as flexible and low-carbon sources of electricity which are important building blocks in terms of the switch to a low-carbon energy generation, we consider the model risk in this asset class in detail. Our findings reveal that spike risk is by far the most important source of model risk.

This talk is based on joint work with Karl Bannör, Rüdiger Kiesel and Matthias Scherer.

Marcus Nossman

Title: A Cointegrated Spot-Swap Model for Power Prices: A Regime Switching Approach with Stochastic Volatility and Jumps

Abstract: We propose a model for the joint evolution of electricity spot and swap prices. The model features several important characteristics observed in power markets; the volatility smile in the swaption market, regime switching behavior and jumps in the spot market and cointegration between spot and swap prices. Estimation is carried out using a time series panel of electricity swaption prices and historical spot prices. The model is able to both accurately price swaptions and represent the dynamics of spot prices. We show how to apply the model to the valuation of virtual power plants, via strips of spot options, in a numerical study.

This talk is based on joint work with Rikard Green and Karl Larsson.

Jakub Nowotarski

Title: Robust estimation and forecasting of the long-term seasonal component of electricity spot prices

Abstract: We present the results of an extensive study on estimation and forecasting of the long-term seasonal component (LTSC) of electricity spot prices. We consider a battery of over 300 models, including monthly dummies and models based on Fourier or wavelet decomposition combined with linear or exponential decay. We find that the considered wavelet-based models are significantly better in terms of forecasting spot prices up to a year ahead than the commonly used monthly dummies and sine-based models. This result questions the validity and usefulness of stochastic models of spot electricity prices built on the latter two types of LTSC models.

This talk is based on joint work with Jakub Tomczyk, Rafal Weron.

Salvador Ortiz-Latorre

Title: A pricing measure to explain the risk premium in power markets

Abstract: In electricity markets, it is sensible to use a two-factor model with mean reversion for spot prices. One of the factors is an Ornstein-Uhlenbeck (OU) process driven by a Brownian motion and accounts for the small variations. The other factor is an OU process driven by a pure jump Lévy process and models the characteristic spikes observed in such markets. When it comes to pricing, a popular choice of pricing measure is given by the Esscher transform that preserves the probabilistic structure of the driving Lévy processes, while changing the levels of mean reversion. Using this choice one can generate stochastic risk premiums (in geometric spot models) but with (deterministically) changing sign. In this talk we introduce a pricing change of measure, which is an extension of the Esscher transform. With this new change of measure we also can slow down the speed of mean reversion and generate stochastic risk premiums with stochastic non constant sign, even in arithmetic spot models. In particular, we can generate risk profiles with positive values in the short end of the forward curve and negative values in the long end. Finally, our pricing measure allows us to have a stationary spot dynamics while still having randomly fluctuating forward prices for contracts far from maturity.

Maria Osipenko

Title: Spatial Risk Premium on Weather Derivatives and Hedging Weather Exposure in Electricity

Abstract: Due to the dependency of the energy demand on temperature, weather derivatives enable the effective hedging of temperature reated fluctuations. However, temperature varies in space and time and therefore the contingent weather derivatives also vary. The spatial derivative price distribution involves a risk premium. We examine functional principal components of temperature variation for this spatial risk premium. We employ a pricing model for temperature derivatives based on dynamics modeled via a vectorial Ornstein-Uhlenbeck process with seasonal variation. We show that in our model risk premia depends on the temperature variation curves in the measurement period. The dependence is exploited by a functional principal component analysis of the curves. We compute risk premia on cumulative average temperature futures for locations traded on Chicago Mercantile Exchange (CME) and fit to it a geographically weighted regression on functional principal component scores. It allows us to predict risk premia for nontraded locations and to adopt, on this basis, a hedging strategy, which we illustrate in the example of Leipzig.

Yoichi Otsubo

Title: Location Basis Differentials in Crude Oil Prices

Abstract: We examine the long-run pricing relationship among crude oil prices at the North Sea (Brent), Cushing (WTI) and Louisiana Gulf (LLS) delivery points. Crude oil prices become non-stationary prior to the …financial crisis. The Brent-WTI location basis differential is stable until the end of 2010, but it widens to record levels in the last two years.

Brent prices adjust to WTI prices prior to August 2008, and then the adjustment process reverses. U.S. retail gas prices respond to Brent and WTI before August 2008 and then only to Brent afterwards. The Brent-LLS cointegration relationship remains stable throughout the sample. We show that the recent Brent-WTI price differential is Granger-caused by Chinese crude oil supplies and shipments out of the Cushing delivery location. We report on recent changes in the supply chain designed to profit from the Brent-WTI gap.

This talk is based on joint work with Yang Li and Bruce Mizrach.

Florentina Paraschiv

Title: Medium-term planning for thermal electricity production

Abstract: In the present paper we present a mid-term planning model for thermal power generation which is based on multistage stochastic optimization and involves stochastic electricity spot prices, a mixture of fuels with stochastic prices, the effect of CO2 emission prices and various types of further operating costs. Going from data to decisions, the first goal is to estimate simulation models for various commodity prices. We apply Geometric Brownian motions with jumps to model gas, coal, oil and emission allowance (EUA) spot prices. Electricity spot prices are modeled by a regime switching approach which takes into account seasonal effects and spikes. Given the estimated models we simulate scenario paths and then use a multiperiod generalization of the Wasserstein distance for constructing the stochastic trees used in the optimization model. Finally, we solve a one year planning problem for a fictitious configuration of thermal units, producing against the markets. We use the implemented model to demonstrate the effect of CO2 prices on cumulated emissions and to apply the indifference pricing principle to simple electricity delivery contracts.

This talk is based on joint work with Raimund M. Kovacevic.

Tommaso Pellegrino

Title: On the Use of the Moment-Matching Technique for Pricing and Hedging Multi-Asset Spread Options

Abstract: It is a common practice among practitioners to model virtual power plants as spread options, where the production cost of a power plant integrate a cost of carbon emissions in addition to the cost of the fuel (normally natural gas in a clean spark spread option). The aim of this paper is to show the benefit of applying a moment matching technique to the fuel leg component (see for example Brigo et al. [2]) in order to price and hedge multi-asset spread options. The main advantage associated with the moment matching approach is that one can continue using all the option formulas available in the literature for simple spread options written on two underlyings (see for example Bjerksund and Stensland [1], Deng et al. [3], Kirk [5] and Ravindran [7]). Besides it, the combined use of an option formula for simple spread options and moment matching technique applied to the fuel leg component provides a good approximation to the Monte Carlo simulation, whose values, price and Greeks, can be considered as the benchmark since no exact formula is available for the pricing and hedging multi-asset spread options. The accuracy is even comparable to the one provided by using closed-form formulas based on three underlyings, as done, for example, in Deng et al. [4] or in Nel [6].

This talk is based on joint work with Piergiacomo Sabino.

[1] P. Bjerksund, G. Stensland, Closed Form Spread Option Valuation, Quantitative Finance, (2011).

[2] D. Brigo, F. Mercurio, F. Rapisarda, et al., Approximated moment-matching dynamics for basket-options pricing, Quantiative Finance, (2004).

[3] S. J. Deng, M. Li, and J. Zhou. Closed-form approximations for spread option prices and Greeks, Journal of Derivatives, 58-80, (2008).

[4] S. J. Deng, M. Li, and J. Zhou, Multi-asset Spread Option Pricing and Hedging, Quantitative Finance, (2010).

[5] E. Kirk, Correlations in the energy markets, Managing Energy Price Risk. Risk Publications and Enron, 71-78, London (1995).

[6] D. Nel, Carbon Trading, thesis submitted for the MSc in Mathematical Finance, University of Oxford, (2009).

[7] K. Ravindran, Low-fat spreads RISK 6 (10) 56-57, (1993).

Wolfgang Raabe

Title: Calculation of Monte Carlo Sensitivities for a portfolio of time coupled options subject to external constraints

Abstract: We calculate robust Monte-Carlo sensitivities (Deltas and Gammas) for a portfolio of complex options which are subject to typical power plant related constraints like minimum/maximum load and minimum up- and down time. We overcome well known numerical performance problems of Monte-Carlo second derivatives by applying the Proxy Simulation Scheme method of Fries and Kampen (2006) which effectively recycles Monte-Carlo realisations.

This approach allows us to study the impact of reserve energy requirements on the value and risk profile of a stylised power plant option portfolio. In particular, we are able to derive hedge parameters for reserve contracts which is a common challenge for utilities.

Eran Raviv

Title: An empirical comparison of alternate schemes for combining electricity spot price forecasts

Abstract: In this paper we investigate the use of forecast averaging for electricity spot prices. While there is an increasing body of literature on the use of forecast combinations, there is only a small number of applications of these techniques in the area of electricity markets. In this comprehensive empirical study we apply seven averaging and one selection scheme and perform a backtesting analysis on day-ahead electricity prices in three major European and US markets. Our findings support the additional benefit of combining forecasts for deriving more accurate predictions, however, the performance is not uniform across the considered markets. Interestingly, equally weighted pooling of forecasts emerges as a viable robust alternative compared with other schemes that rely on estimated combination weights. Overall, we provide empirical evidence that also for the extremely volatile electricity markets, it is beneficial to combine forecasts from various models for the prediction of day-ahead electricity prices. In addition, we empirically demonstrate that not all forecast combination schemes are recommended.

This talk is based on joint work with Jakub Nowotarski, Stefan Trück and Rafał Weron.

Philipp Ringler

Title: Accounting for Real Options in Power Plant Investments using an Agent-Based Simulation Model of Electricity Markets

Abstract: Investments in electricity generation assets exhibit different types of real options. With regard to the mid- and long-term development of electricity markets, it is particularly relevant to consider early power plants closures within electricity market models. Therefore, we propose in this paper an extension of an existing agent-based simulation model which allows individually modeled agents to determine their optimal policy regarding timing and scope of investment decision. Based on a discrete-time multi-stage stochastic expansion planning approach, the effect of early plant closures on power prices and generation adequacy is expected to be analyzed. The consideration of long-term uncertainties allows simulating investment behavior under respective conditions.

This talk is based on joint work with Massimo Genoese, Wolf Fichtner.

Piergiacomo Sabino

Title: Enhancing Least Squares Monte Carlo with Diffusion Bridges: an Application to Virtual Hydro Power Plants

Abstract: The aim of this study is to present an efficient and easy framework for the application of the Least Squares Monte Carlo methodology to gas or power facilities as detailed in Boogert and de Jong [1]. As mentioned in the seminal paper by Longstaff and Schwartz [3], the convergence of the Least Squares Monte Carlo depends on the convergence of the optimization combined with the convergence of the pure Monte Carlo method. In the context of the energy facilities, the optimization is more complex and its convergence is of fundamental importance in particular for the computation of the sensitivities and the optimal dispatched quantities. To our knowledge, an extensive study of the convergence and hence, of the reliability of the algorithm has not been performed yet, in our opinion because of the apparent infeasibility and complexity to use a very high number of simulations. We present then an easy way to simulate random trajectories by means of diffusion bridges similar to the one proposed by Kutt and Welke [2]. The strategy of simulating trajectories backward in time can be seen in the context of time reversal Itˆo diffusions or in the context of the exact simulation of stochastic differential equations. Our approach permits to perform a backward dynamic programming strategy based on a huge number of simulations without storing the simulated trajectories. Generally, in the valuation of energy facilities one is also interested in the forward recursion in order to get the optimal dispatched strategy. We then design the backward and forward recursions such that one can produce the same random trajectories by the use of multiple independent random streams without saving the intermediate time steps prices once more. Finally, we show the practical advantages of our methodology for the valuation of virtual hydro power plants.

This talk is based on joint work with Tommaso Pellegrino.

[1] A. Boogert and C. de Jong. Gas Storage Valuation Using a Monte Carlo Method. Journal of Derivatives, 15:81–91, 2008.

[2] S.K. Dutt and G.M. Welke. Just in Time Monte Carlo for Path Dependent American Options. The Journal of Derivatives, Vol. 15, No. 4:29–47, 2008.

[3] F. A. Longstaff and E.S. Schwartz. Valuing American Options by Simulation: a Simple Least- Squares Approach. Review of Financial Studies, pages 113–147, 2001.

Franziska Schulz

Title: Forecasting generalized quantiles of electricity demand: A functional data approach

Abstract: Electricity load forecasts are in various ways valuable for the operation of utilities. However, for a sustainable risk management of utility operators not only a forecast of expected demand, but also knowledge about the uncertainty and dispersion of future load plays an important role. The aim of our research is to model and forecast generalized quantiles of electricity demand, which, in contrast to forecasts of the conditional mean, yield a whole picture of the distribution of electricity demand. We apply methods from functional data analysis to model dynamics of daily generalized quantile curves. Taking temporal dependence between curves into account allows us to conduct short term forecasts at an intraday resolution using multivariate time-series techniques.

Michael Schürle

Title: Price dynamics in gas markets

Abstract: Modeling natural gas futures prices is essential for valuation purposes as well as for hedging strategies in energy risk management. We present a general multi-factor affine diffusion model which incorporates the joint stylized features of both spot and futures prices. The model is brought into state space form on which Kalman Filter techniques are applied to evaluate the maximum likelihood function. We further build the basis for the construction of a daily gas price forward curve. These prices take into account the seasonal structures of spot prices and are consistent under the arbitrage-free condition with the observed market prices of standard products that provide gas delivery over longer periods. Finally the performance of the models is illustrated comparing historical and model implied price characteristics.

Pierre Six

Title: Convenience Yield and Adjusted Basis Stylized Facts

Abstract: This article examines the theory of storage in directly considering the convenience yield. Indeed, other empirical studies focus on the risk adjusted basis of commodity prices to analyze the stylized facts of storable commodities. However, we show in this article that this basis is unlikely to be a good proxy for the convenience yield. We run a first qualitative analysis for oil and copper and prove that the stylized facts predicted by the theory of storage are much more validated when the convenience yield is considered as opposed to the risk adjusted basis.

This talk is based on joint work with Julien Fouquau.

Stefan Trück

Title: How is Convenience Yield Risk Priced?